Kao

Kao has long been a leader in business execution and capital management. In 1999, the company announced that “Kao aims to maximize shareholder value. At the same time, we realize that this will also serve to increase the value of the company for other stakeholders.” Kao’s consistent commitment to creating value for stakeholders has been rewarded with a premium valuation relative to both domestic and foreign peers. This premium valuation opens up a number of strategic options to the company and positions it to build on its success.

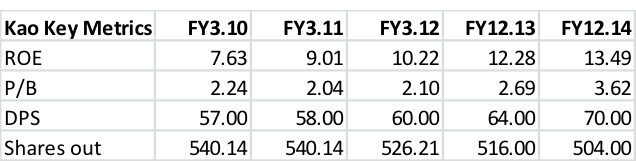

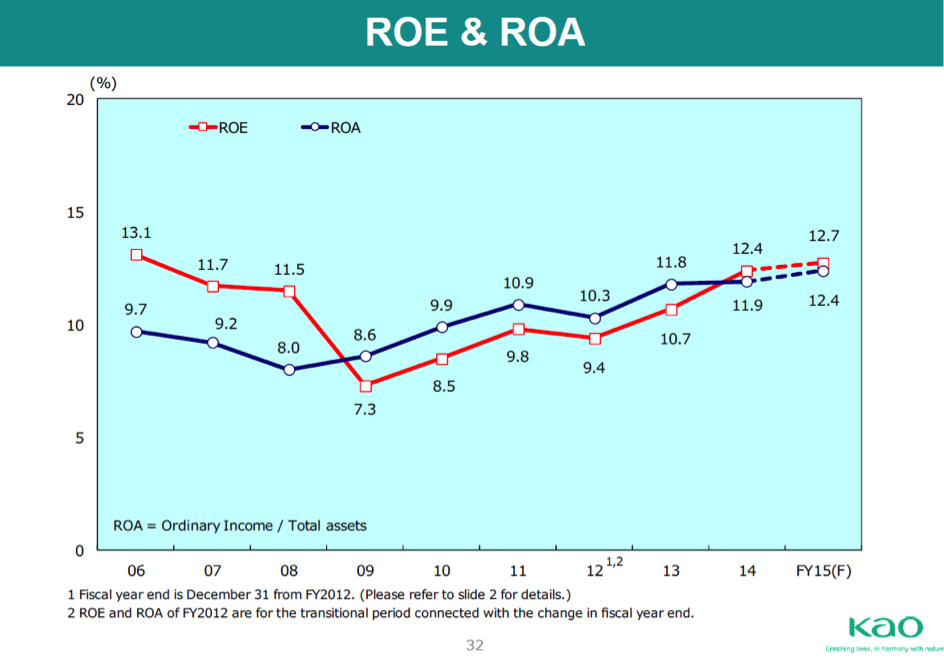

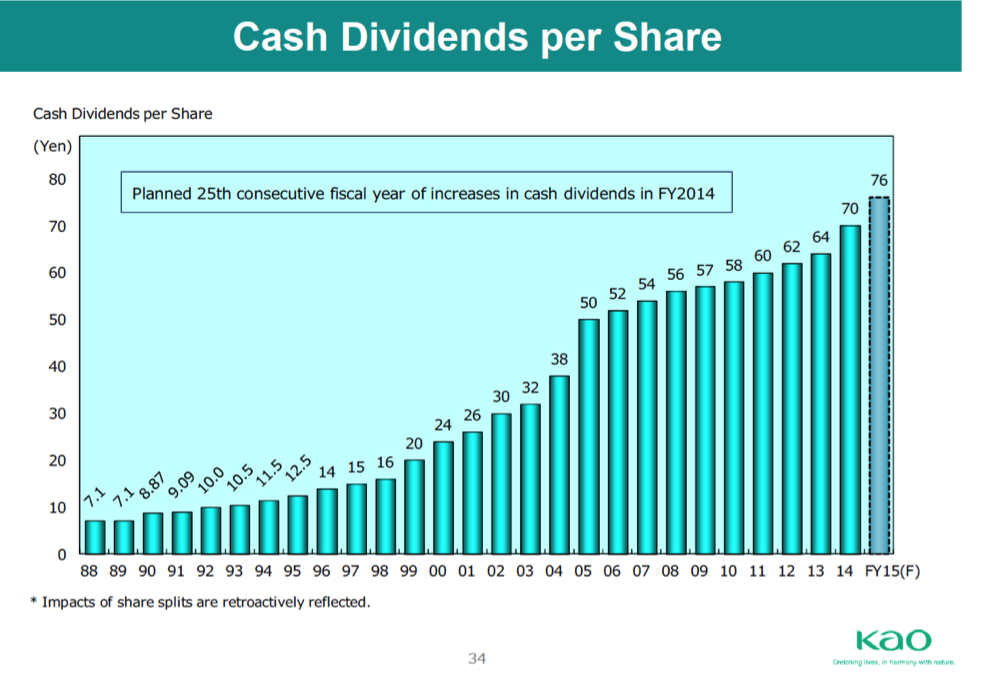

Kao has consistently improved ROE, reduced shares outstanding, and increased dividends per share:

Sources: company reports, Bloomberg

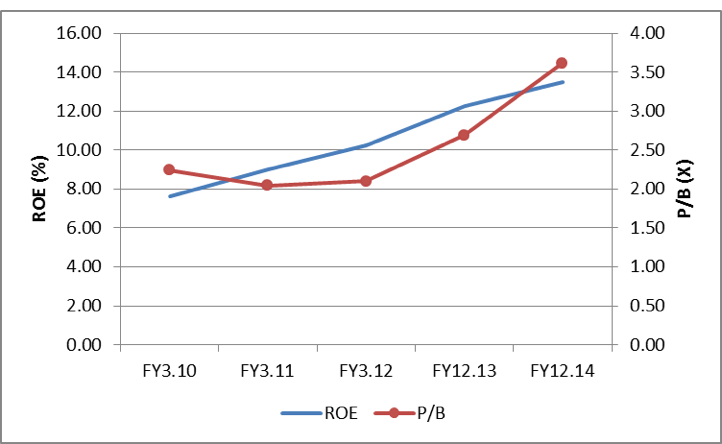

Kao’s strong commitment to increasing ROE and returns to shareholders has been rewarded with an expanding P/B ratio:

Sources: company reports, Bloomberg

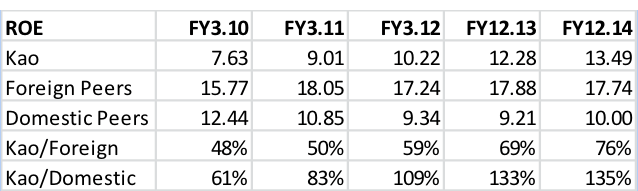

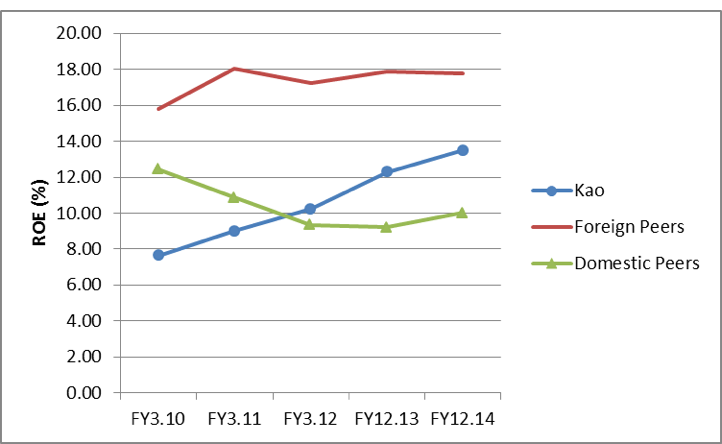

Kao has continuously improved its ROE relative foreign and domestic peers:

Sources: company reports, Bloomberg

Sources: company reports, Bloomberg

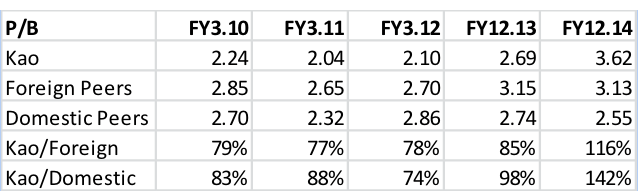

Kao now commands a substantial valuation premium to both foreign and domestic peers:

Sources: company reports, Bloomberg

Sources: company reports, Bloomberg

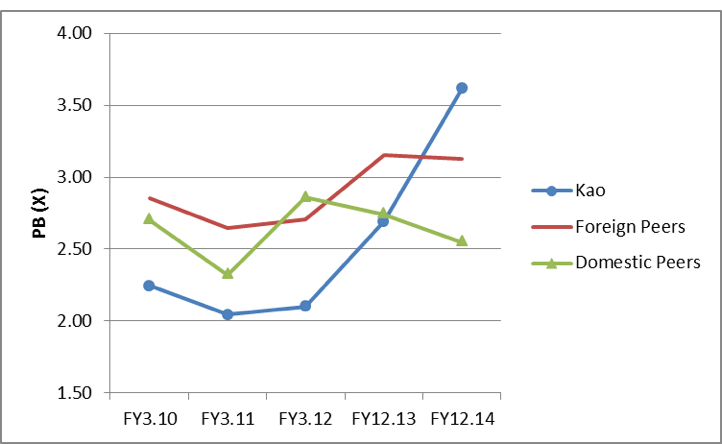

Kao continuously improved ROE through higher asset turns (increasing revenues relative to assets) and improved profit margins. Despite stock buybacks and increased dividends, leverage (assets to equity) still decreased:

Sources: company reports, Bloomberg

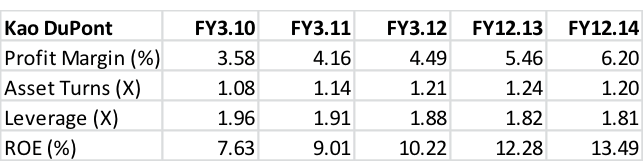

Kao communicates clearly regarding its commitment to efficient capital management and returns to shareholders:

Source: company reports

Source: company reports

Source: company reports

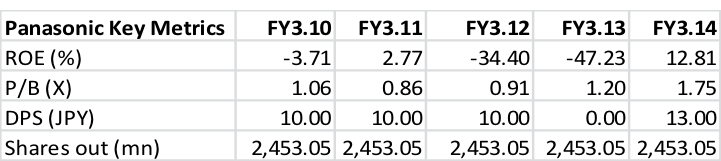

Panasonic

Panasonic has a long history of cost efficiency, but has emphasized and accelerated its commitment to shareholders through an effective and comprehensive business restructuring over the last two years.

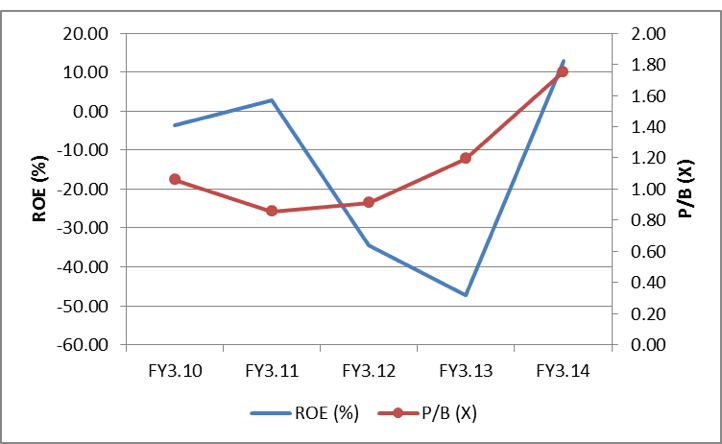

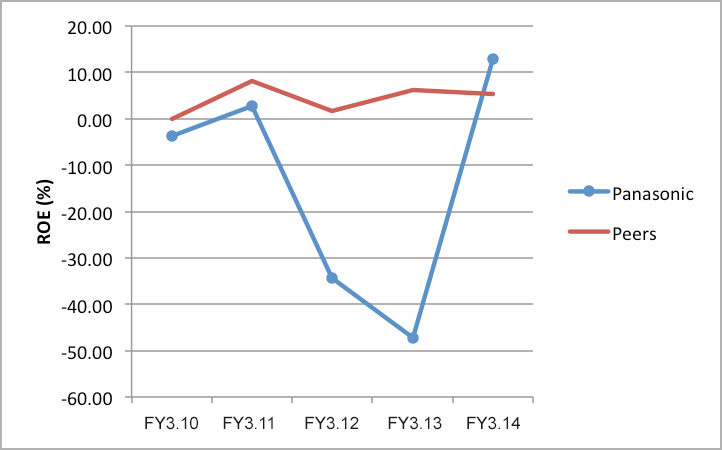

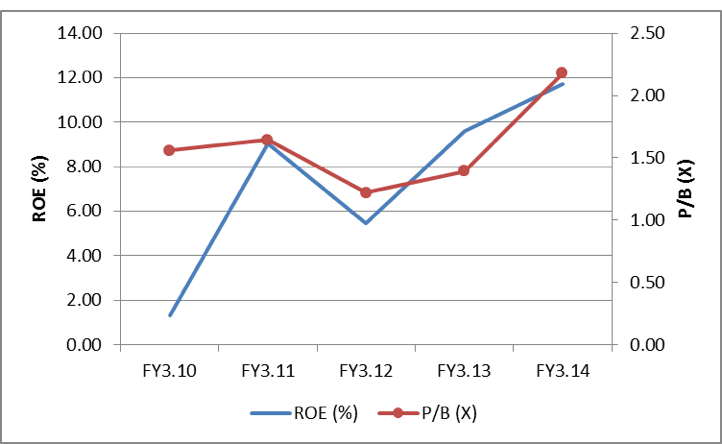

The company has successfully recovered from a lossmaking position and dividend suspension in FY 3/13, with an impressive turnaround in ROE to an all-time high of 10%. This has led to a rerating of the stock, with the P/B ratio recovering from 0.8x to 1.8x.

Sources: company reports, Bloomberg

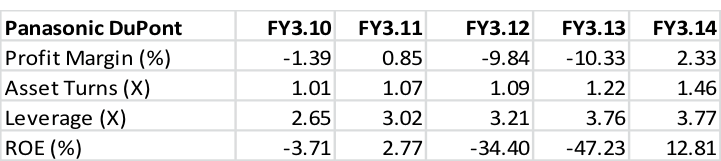

The dramatic improvement in ROE has been driven by all three factors: asset turn, leverage, and margins:

Sources: company reports, Bloomberg

Despite higher leverage, Panasonic is still comfortable re-instating DPS 30% above previous levels:

Sources: company reports, Bloomberg

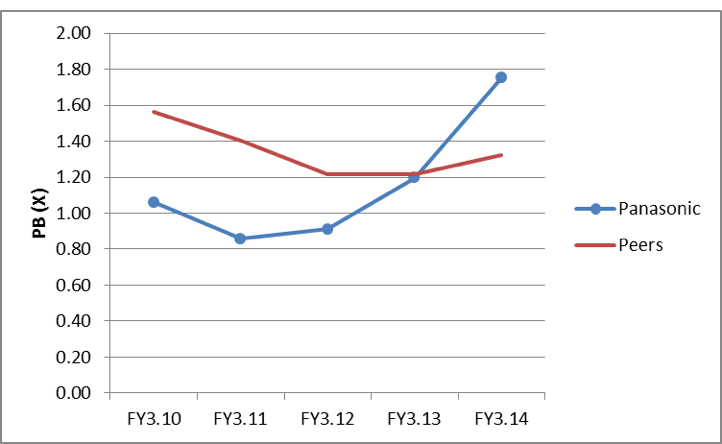

Panasonic now trades at a higher P/B ratio than its peers:

Sources: company reports, Bloomberg

Note: peers are Hitachi, Toshiba, NEC, Mitsubishi Electric, Sony

Because it has a higher ROE:

Sources: company reports, Bloomberg

Note: peers are Hitachi, Toshiba, NEC, Mitsubishi Electric, Sony

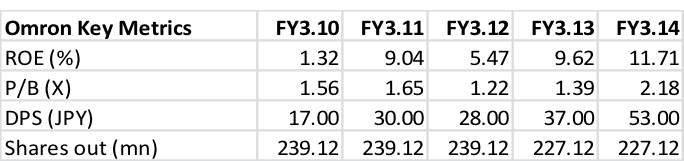

Omron

Omron made a serious commitment to better capital management with the appointment of its first CFO in 2013. The minimum dividend payout ratio was raised from 20 to 25%, with a target of 30% by 2016. At the same time, a commitment was made to conduct share buybacks to reduce the accumulated capital surplus.

ROE has improved from 5.2% to 11.6% in two years, and is forecast to reach 13.9% in FY 3/15 based on consensus estimates. This improvement in ROE and shareholder returns has been rewarded by a rise in Omron’s P/B ratio:

Sources: company reports, Bloomberg

Pledges on payouts have been met: dividends/share have almost doubled,

while the number of shares outstanding has fallen by 5%:

Sources: company reports, Bloomberg

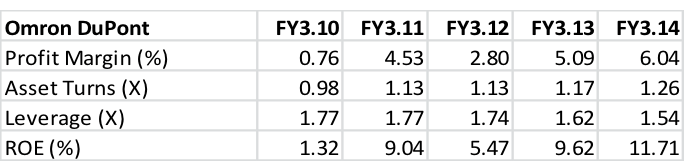

Omron’s ROE has been supported by a more efficient asset turn (sales to total assets).

Despite higher DPS and share buybacks, leverage has also fallen.

Sources: company reports, Bloomberg

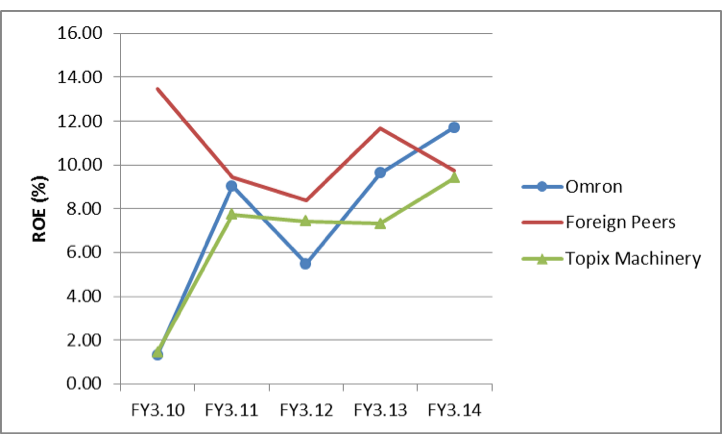

Omron’s ROE now exceeds that of both domestic and global peers:

Sources: company reports, Bloomberg

Note: Foreign peers are Siemens and Philips

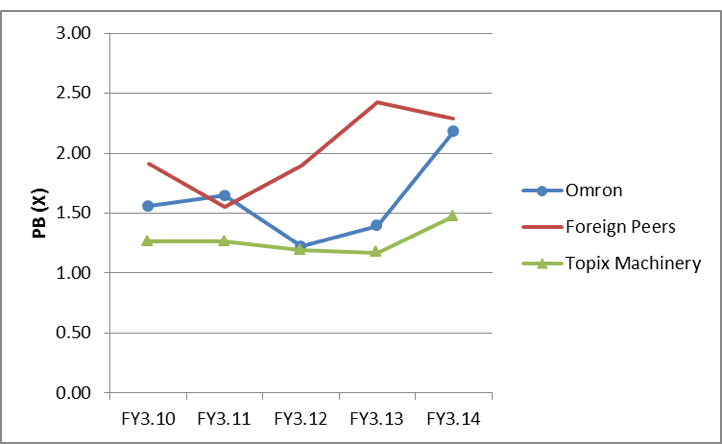

This improvement has been reflected in a commensurate rise in PB/ratio to

match that of comparable global companies:

Sources: company reports, Bloomberg

Note: Foreign peers are Siemens and Philips

Mabuchi Motors

In 2008 and 2009, Mabuchi initiated a meaningful share buyback program at attractive prices. Since then, the company has continued to buy back shares and increased dividends per share substantially. ROE has improved considerably, and Mabuchi’s price to book ratio has improved from less than one third that of peer companies to a much smaller 20% discount.

Mabuchi has consistently improved ROE, reduced shares outstanding, and increased dividends per share:

Sources: company reports, Bloomberg

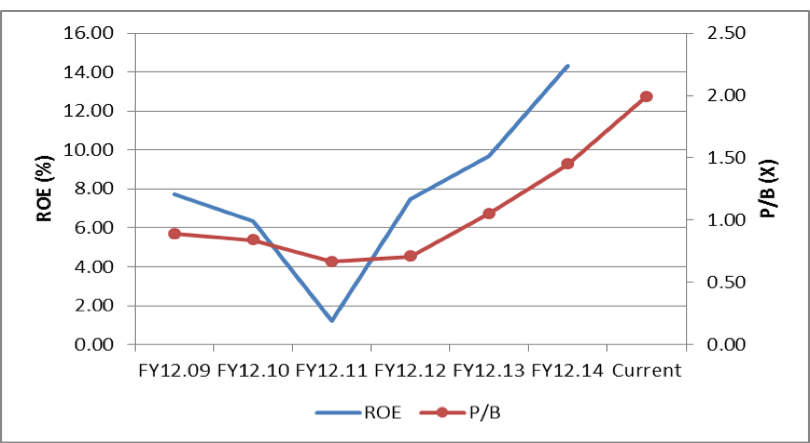

Mabuchi’s ROE and P/B have both doubled since 2009:

Sources: company reports, Bloomberg

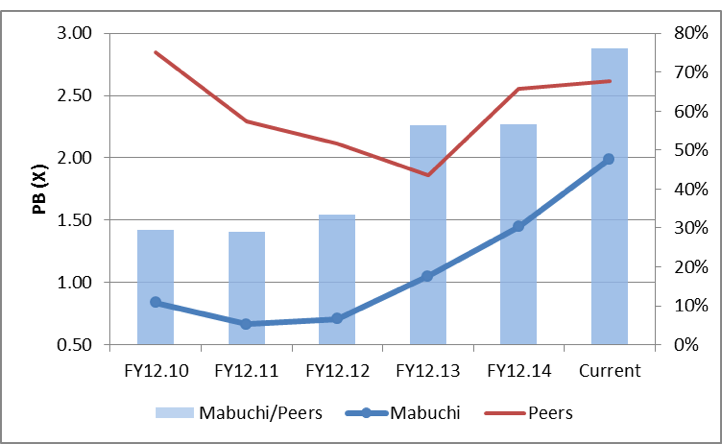

Mabuchi has consistently narrowed its valuation gap relative to global peers:

Sources: company reports, Bloomberg

Note: peers are Nidec, Yaskawa Electric, and Johnson Motors

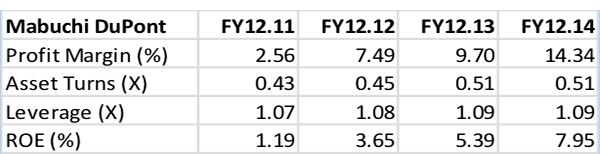

Mabuchi’s consistent capital management policy has improved ROE and asset turn (sales to total assets) while maintaining modest financial leverage (assets to equity):

Sources: company reports, Bloomberg

Amada

Amada introduced investor-friendly policies at the start of FY3/15. Policies include a 50% dividend payout ratio, buying back and retiring 10 million shares (2.6% of total shares outstanding at the start of FY3/15) and an ultimate ROE target of 10% (7% in FY3/15). Investors have responded favorably to these policies, and Amada’s valuation has risen from less than half that of its peers to industry averages.

Amada’s P/B expanded from 0.6x, generally regarded as selling below replacement value, to a premium to book value following the announced commitment to enhanced capital management:

Sources: company reports, Bloomberg

Note: forecast ROE is based on Bloomberg consensus estimates

Amada’s ROE is expected to remain below the level of peer companies:

Sources: company reports, Bloomberg

Note: forecast ROE is based on Bloomberg consensus estimates

But the company’s clear commitment to improved capital management has narrowed the gap between its valuation and peer companies from 65% to 30%:

Sources: company reports, Bloomberg

Note: forecast ROE is based on Bloomberg consensus estimates

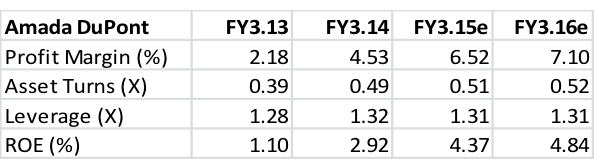

Amada’s announced policies are expected to increase asset turn (revenues to total assets) and stem the decline in leverage (assets to equity), raising ROE:

Sources: company reports, Bloomberg

Note: forecast ROE is based on Bloomberg consensus estimates

Tokio Marine

Tokio Marine made a significant commitment to shareholder returns and capital management in its three year mid-term plan which began in 2011. At that time the company targeted a FY ROE of 7.4% (from -0.7%), a target dividend payout ratio of 40-50% of average adjusted earnings, and flexible share buybacks. Tokio Marine undertook to achieve higher shareholder returns and payouts through improved capital efficiency and increased profitability, underpinned by a commitment to financial soundness.

FY3/14 ROE surpassed the initial target level, and DPS has increased by 40% in two years. Meanwhile, shares outstanding have fallen by 4.5%. In the second half of FY2014, the company resolved to buy back up to Y50B of shares, and has committed to maintaining an appropriate level of capital through further buybacks.

Source: company reports, Bloomberg

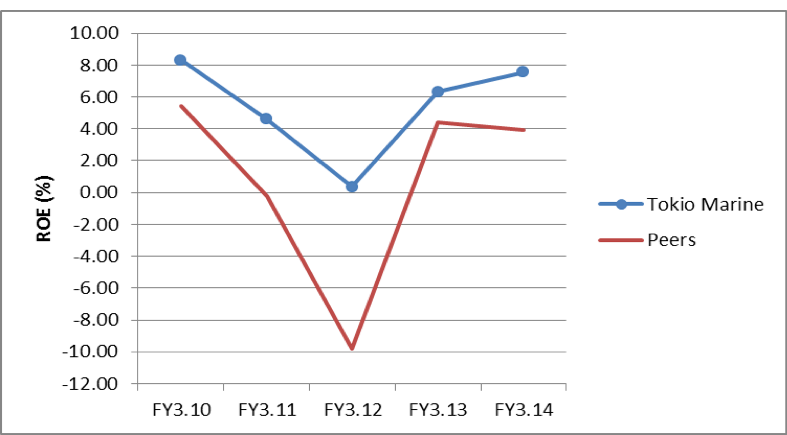

Tokio Marine has consistently earned a higher ROE than peers:

Source: company reports, Bloomberg

Note: peers are MS&AD and Sompo

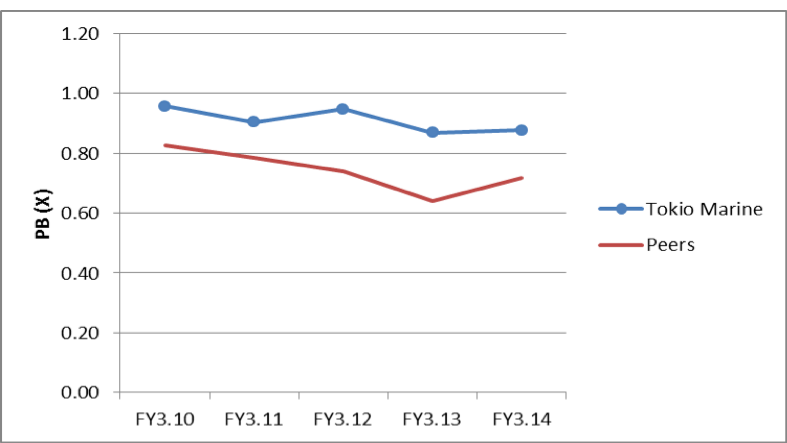

Thanks to its higher ROE and clear commitment to efficient capital management, the company has maintained a valuation premium over its peers:

Source: company reports, Bloomberg

Note: peers are MS&AD and Sompo

Izumi

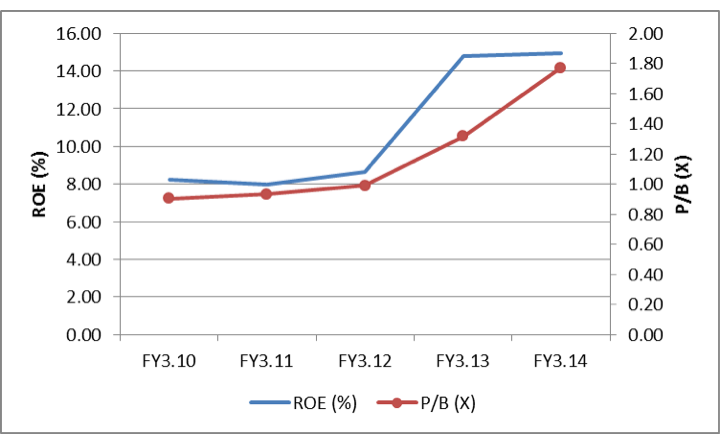

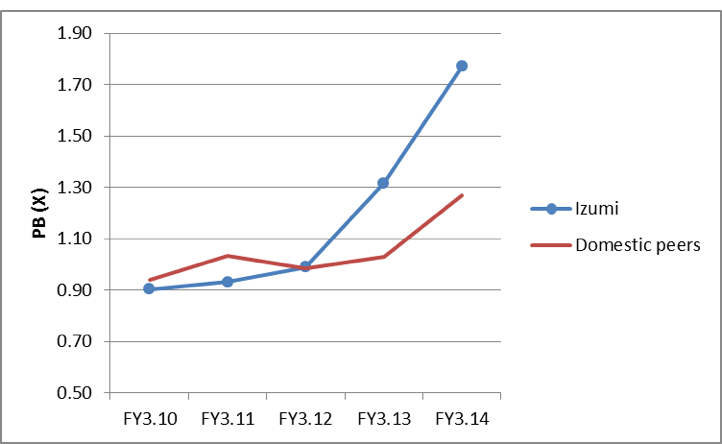

In 2011 Izumi began returning surplus funds to shareholders via buybacks and higher dividends. A steady improvement in ROE has driven a doubling of its price to book ratio. The company now commands a large valuation premium to its domestic peers.

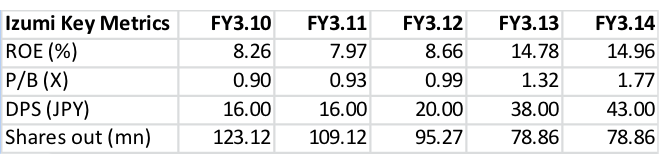

Consistent capital management policy has led to a 35% reduction in shares outstanding and a 170% increase in DPS from 2010 to 2014:

Source: company reports, Bloomberg

Izumi’s P/B ratio has nearly doubled as the company’s ROE improved:

Source: company reports, Bloomberg

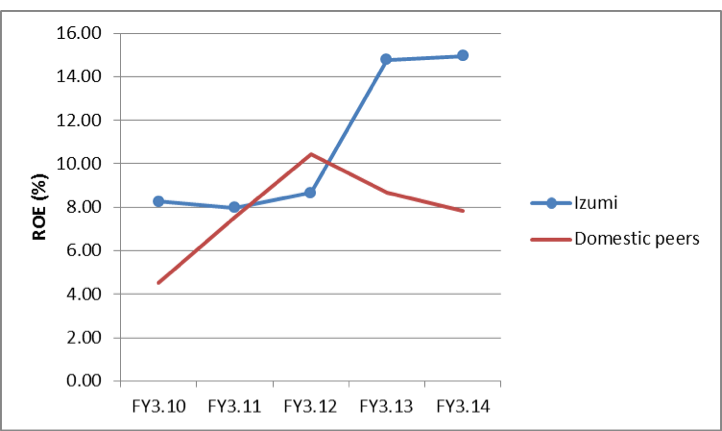

ROE now far outstrips leading domestic peers:

Source: company reports, Bloomberg

Domestic peers: Aeon and Seven & I Holdings

Izumi now enjoys a meaningful valuation premium to its peers:

Source: company reports, Bloomberg

Domestic peers: Aeon and Seven & I Holdings

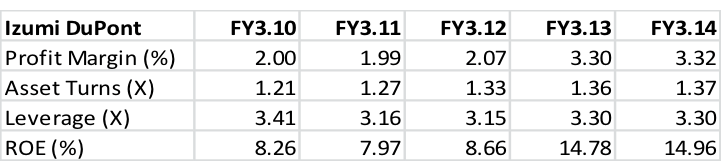

Consistent capital management policy has improved both ROE and asset turn (sales to total assets) while decreasing financial leverage:

Source: company reports, Bloomberg

0 Comments